Results of the ECB 2022 climate risk stress test

The first supervisory climate risk stress test (2022 CST) conducted by the European Central Bank (ECB) has concluded with official results and findings made public on 8 July 2022. The exercise has complemented the broader ECB’s agenda to assess the readiness of banks in Europe to manage climate-related and environmental risks. The 2022 CST was a novel and challenging exercise for many participants. The results revealed that banks, despite making meaningful progress, do not yet fulfil ECB’s expectations on incorporating climate risk into their respective stress-testing frameworks and internal models.

Results

The 2022 CST results revealed that banks, despite making meaningful progress, do not yet fulfil ECB’s expectations on incorporating climate risk into their respective stress-testing frameworks and internal models. Multiple deficiencies, data gaps and inconsistencies were identified across institutions:

- According to the ECB, 60% of sampled banks do not yet have a well-integrated climate risk stress-testing framework, and the majority expect that incorporating physical and/or transition climate risk will be achieved in the medium to long-term. Banks with more developed climate stress-testing frameworks include climate-related and environmental events in their operational risk stress-testing or scenario analysis frameworks; the inclusion of reputational risk is less common.

- The ECB expects banks to perform further work on gathering and managing data with climate-relevant granularity. Most banks made extensive use of proxies instead of actual counterparty data on emissions (especially on Scope 3) and energy performance certificates.

- Long-term strategies for credit allocation policies across transition paths are either not defined or not clearly defined. Banks are advised to step-up their long-term strategic planning and target setting on green transition.

- Credit risk models require further developments as current credit risk parameters projected by banks are insensitive to climate risk shocks provided in scenarios.

- Overall, climate risks are relevant to the sampled banks. The share of interest income related to carbon-intensive industries (22 NACE industries) exceeds 60% of total non-financial corporate interest income and could be a source of significant transition risks to the banks. With regards to physical risks such as drought and heat events and flood risk, some banks are exposed to non-negligible losses depending on the geographical location of their lending activities.

- Combined credit and market losses for Module 3 participants (bottom-up stress test) under the short-term transition risk and two physical risk scenarios were projected at approximately EUR 70 billion and are underestimated in the ECB’s view. According to the ECB, this is due to the nature of the scenarios (no economic downturn assumed), deficient data and modelling underlying the provided projections, no use of supervisory overlays, and studied exposures limited to around one-third of the total exposures of sampled banks.

- With regards to long-term scenarios, the general message is that losses are projected to be lower under the orderly transition scenario in comparison with the disorderly and hot house scenarios.

- Independence between development and validation is only assured by 25% of banks that have climate risk stress-testing frameworks in place. The internal audit function is not yet active on framework review in 40% of banks.

- Pillar III disclosures are not yet common across the sample, with 60% of banks with a climate risk stress-testing framework not making or not planning to make such disclosures.

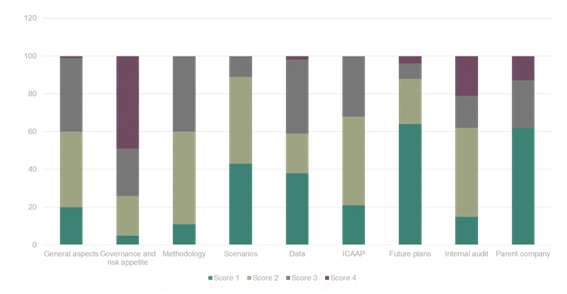

Graphic 1. Preparedness* across key components of climate risk stress-testing frameworks

*ECB scoring: 1 – the best, 4 – the worst

Source: ECB

Background

The 2022 CST exercise aimed to explore climate-related and environmental risks to the financial sector as set out in the ECB’s Banking Supervision strategic priorities. In addition to the ongoing supervisory thematic review of banks’ climate-related and environmental risk management practices, the 2022 CST sought to indicate the extent to which banks fulfil the set of supervisory expectations outlined in the Guide on climate-related and environmental risks published in November 2020.

The ECB assessed the internal climate risk stress-testing capabilities of banks and explored the progress made by banks in developing climate risk stress-testing frameworks, their capacity to incorporate climate risk factors and produce climate stress test projections, and the extent to which banks are facing transition and physical risks as defined in the scenarios provided by the ECB.

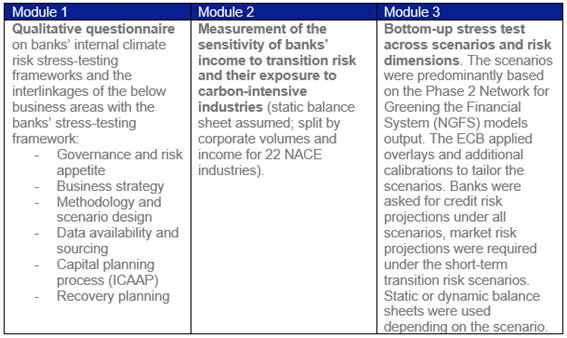

The exercise consisted of three modules, (i) a questionnaire on banks’ climate stress test capabilities, (ii) a peer benchmark analysis to assess the sustainability of banks’ business models and their exposure to emission-intensive companies, and (iii) a bottom-up stress test (see table 1). From both qualitative and quantitative information provided by banks, the ECB analysed:

- Banks’ governance of climate-related and environmental risks

- Availability of relevant data

- Adequacy of transmission channels

- Scenario development capacity

- Coverage of different asset classes

- Sectoral income concentrations

- Financed greenhouse gas (GHG) emissions

- Stress test projections

The ECB applied the proportionality principle when deciding which modules each participating bank has to perform. As a result, from the pool of 104 participants, 41 were chosen to take part in the bottom-up stress test. Participating banks were asked to follow a predefined common methodology published in October 2021, and to provide data and projections under a set of climate risk scenarios published in January 2022. The ECB, similarly to the PRA Climate Biennial Exploratory Scenario exercise conducted in 2021, approached its first supervisory climate risk stress test from an exploratory and learning angle. For this reason, the quality assurance process was less intrusive when compared with the regular EU-wide solvency stress test, and the results did not translate into direct capital requirements.

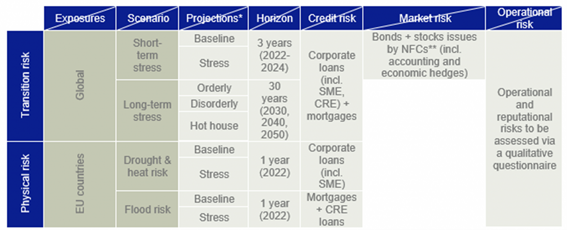

Table 1. Coverage by moduleTable 2. ECB’s overview of scenarios and risk dimensions

Further remarks

On 4 July the ECB reassured the European Parliament of its commitment to further incorporating climate change considerations into its monetary policy framework, banking supervision, financial stability, economic analysis, statistical data and corporate sustainability, within its mandate. The conclusion of the 2022 CST acted as a step on the ECB’s roadmap for stepping up its involvement in climate-related matters. The ECB announced its decision to account for climate change in its corporate bond purchases, collateral framework, disclosure requirements and risk management.

As with regards to 2022 CST follow-up actions, the ECB will summarise good practice in climate risk stress testing to guide institutions that are less advanced on the subject. In its view, some of the participating banks performed visibly better and the industry should learn from current best practices. The ECB observed good performance in engaging with customers to obtain climate-relevant counterparty-level data breakdowns, integration of climate risk into ICAAP, proper climate risk credit modelling capabilities, proper allocation of income and exposure by sector and country, and emission intensity using counterparty-level data, use of proper, actual modelled data to account for the full Scope 3 emissions, and well elaborated green transition plans with well-defined transition targets and KPIs.

The ECB recommendations are expected to go public in the second half of 2022. In parallel to this development, the ECB’s Supervisory Review and Evaluation Process (SREP) will integrate the ongoing Thematic review on climate-related and environmental risk with the 2022 CST findings and communicate the results to individual banks.

Contactar